Empowering America's Financial Journey 2023

How people save, invest, and get advice

About the study

The past year has been trying for many Americans. Disruptive economic and financial conditions have put considerable pressure on day-to-day finances, making it hard for many to pursue their longer-term goals. At the same time, Americans are also benefiting from higher account savings rates, a rebounding equity market from 2022 (although still marked by volatility), and a strong employment market that defies expectations.

These factors are affecting Americans differently, however, making it difficult for some to assess their financial situations and retirement readiness.

The third annual Empowering America’s Financial Journey (EAFJ) study offers an account of how Americans are progressing on their journeys to financial freedom. This year’s study is structured in four chapters:

- American workers under pressure: Are they thriving or treading water?

- A spotlight on retirement preparations across racial/ethnic groups

- Understanding retirement savers and planners

- The final stretch: How Americans are planning for retirement

The 45-page study is based on an analysis of 5.3 million active corporate defined contribution participants with Empower as the recordkeeper. It also incorporates the findings from a survey of 2,511 Americans’ attitudes, confidence, and sentiments related to retirement planning. Throughout the study, we refer to survey respondents interchangeably as “survey respondents” and “Americans” to correspond with the representative sample of polled working Americans.

Americans are taking prudent financial steps to manage the ongoing impact of inflation

While the rate of inflation has declined, overall consumer prices haven’t moved in tandem. As a result, Americans are still taking actions to manage inflation’s impact, including creating a budget, cutting back on daily expenses, and seeking alternate income streams (i.e., “side hustles”).

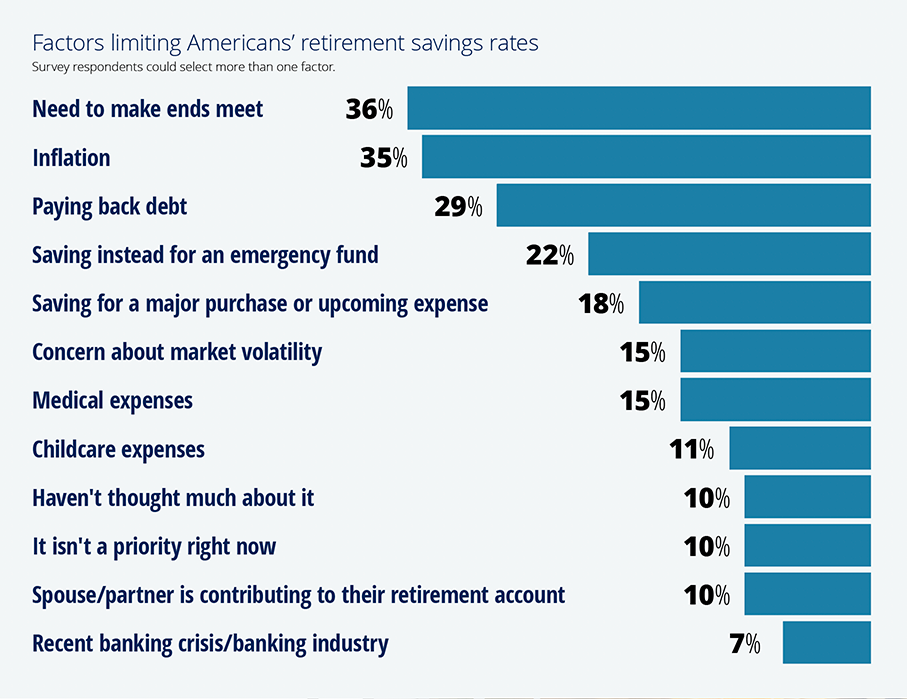

Retirement plan savings rates are staying steady, but only 11% of workplace savers feel they are saving enough

The average retirement plan savings rate has stayed steady at approximately 8%, and more Americans plan to increase rather than decrease their contribution rates. However, the current environment is limiting greater savings. What’s specifically holding workplace savers back? Needing to make ends meet, inflation, and paying back debt.

Loan and hardship withdrawals increasing

New loans and hardship withdrawals taken in each quarter of 2023 were higher than in the past eight quarters. Over the past year, the proportion of workplace savers taking a loan went up by 14%, and the proportion of workplace savers taking a hardship withdrawal went up by 46%. Looking forward, more than one-quarter of working Americans say they are very (10%) or somewhat likely (17%) to take a loan or hardship withdrawal in the next six months.

Download the study to learn more

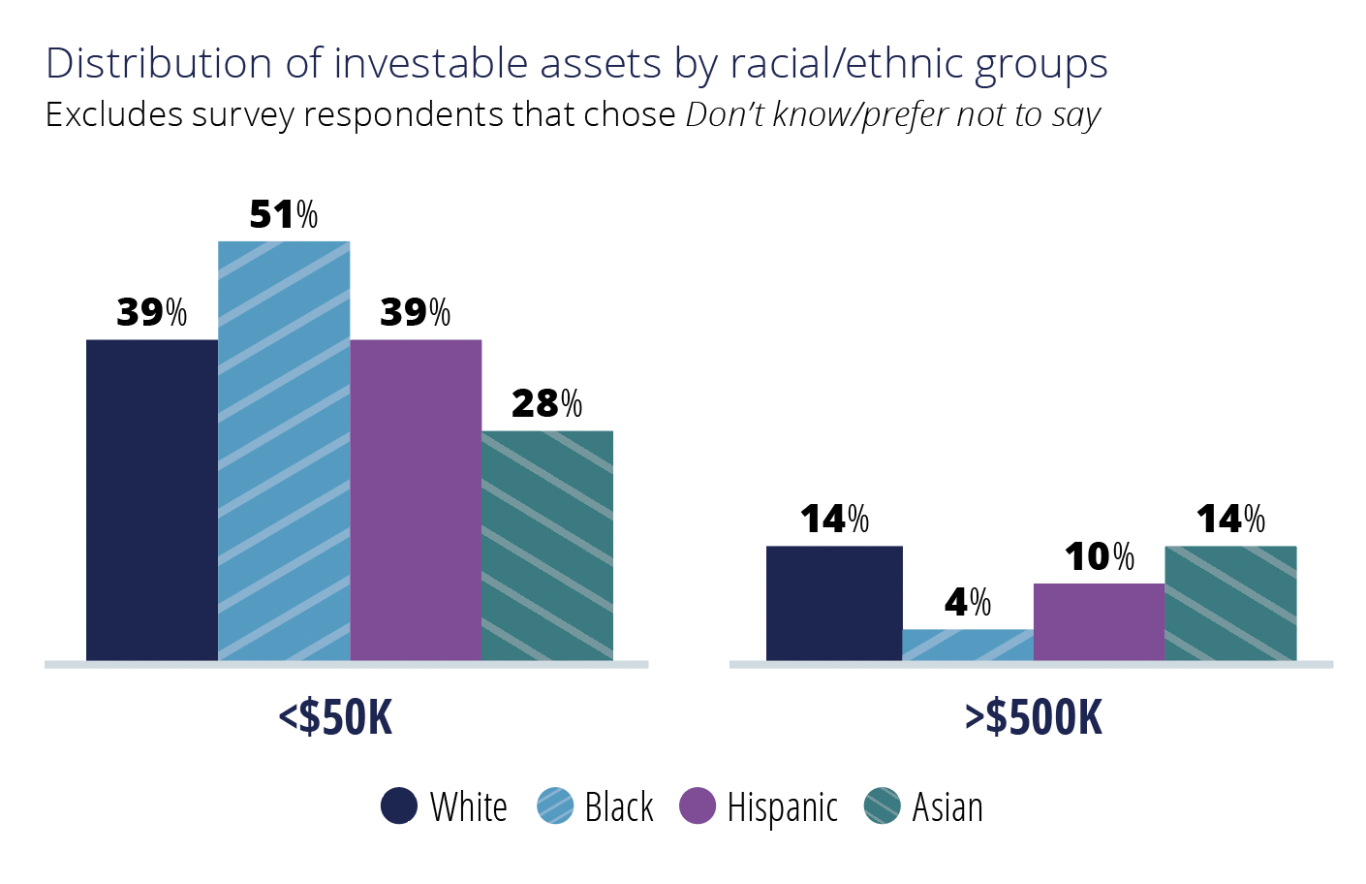

Despite shared financial optimism across racial/ethnic groups, significant wealth gaps exist

Two-thirds or more of white, Black, Hispanic, and Asian Americans are confident they are financially ready for retirement. Yet, there are notable 401(k) savings and investable asset gaps across these demographic groups. Black Americans are significantly underrepresented in the highest wealth segments, and 43% of Hispanic women are saving less than 3% or nothing at all in their workplace defined contribution plans.

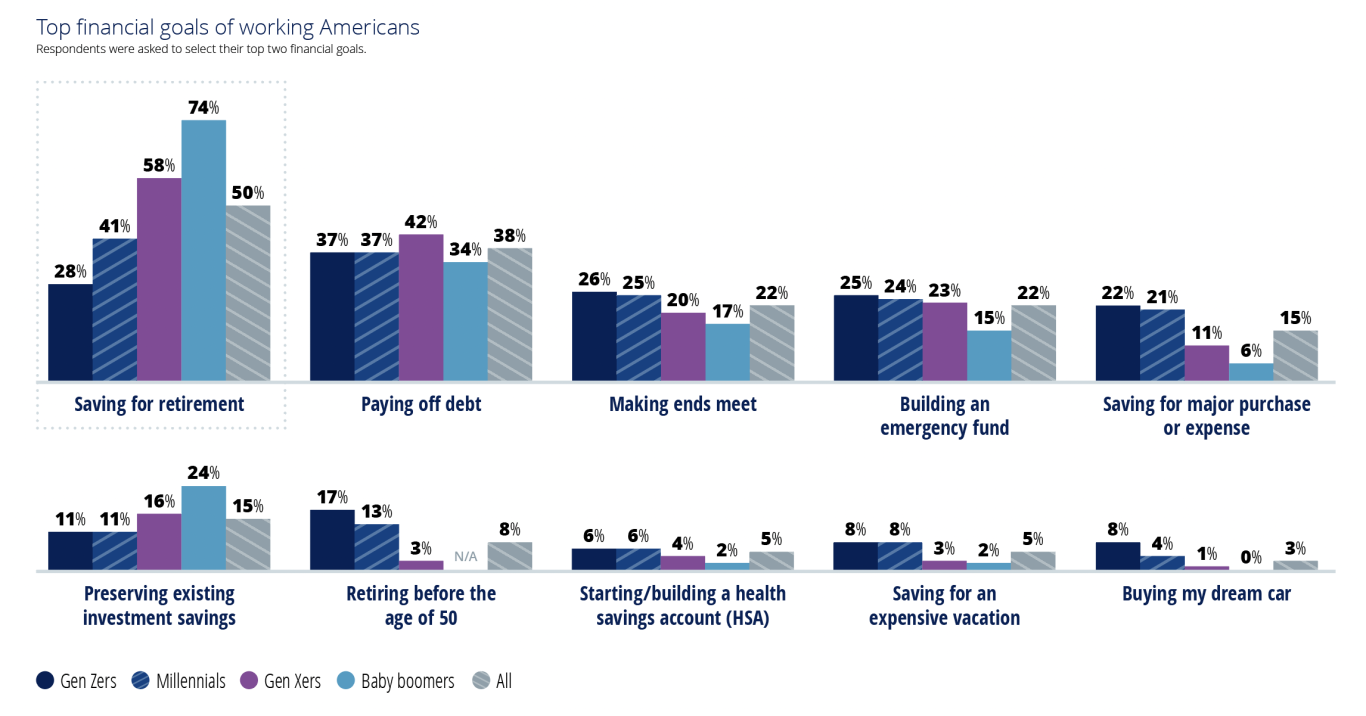

Saving for retirement is the most common financial goal for Americans

Paying off debt and making ends meet tied with building an emergency fund to round out the top three categories.

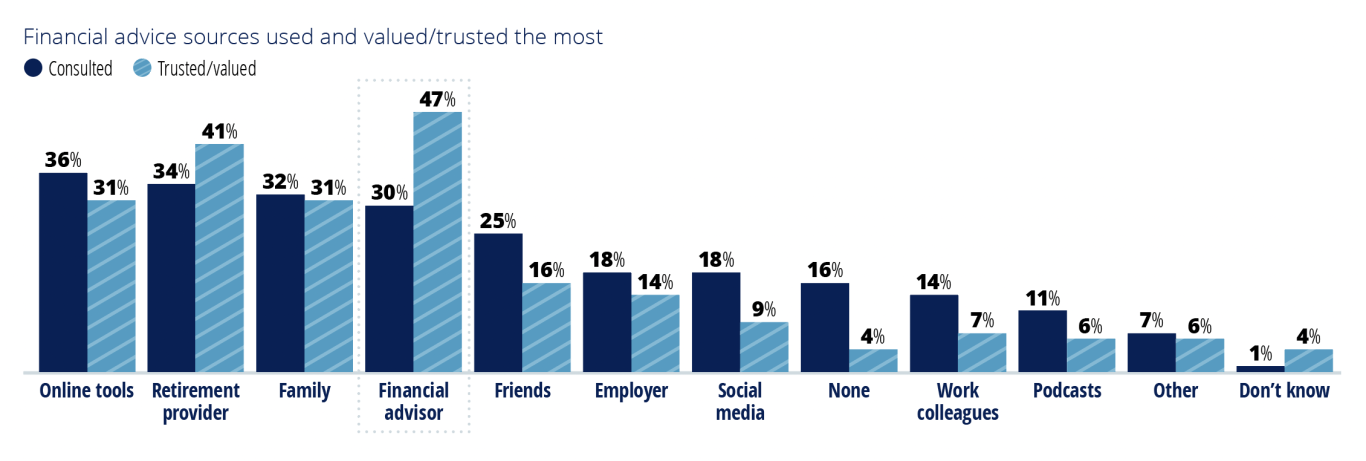

The diversity of advice sources used and trusted by workplace savers illustrates the demand for choice

Working Americans turn to a variety of sources for financial help. Utilization and trust do not always align, however. Almost half of working Americans point to a financial advisor as the most trusted advice source, but only 30% used one in the prior year. A similar but opposite relationship applies to social media sources: While 18% used them, only 9% say they trust or value them.

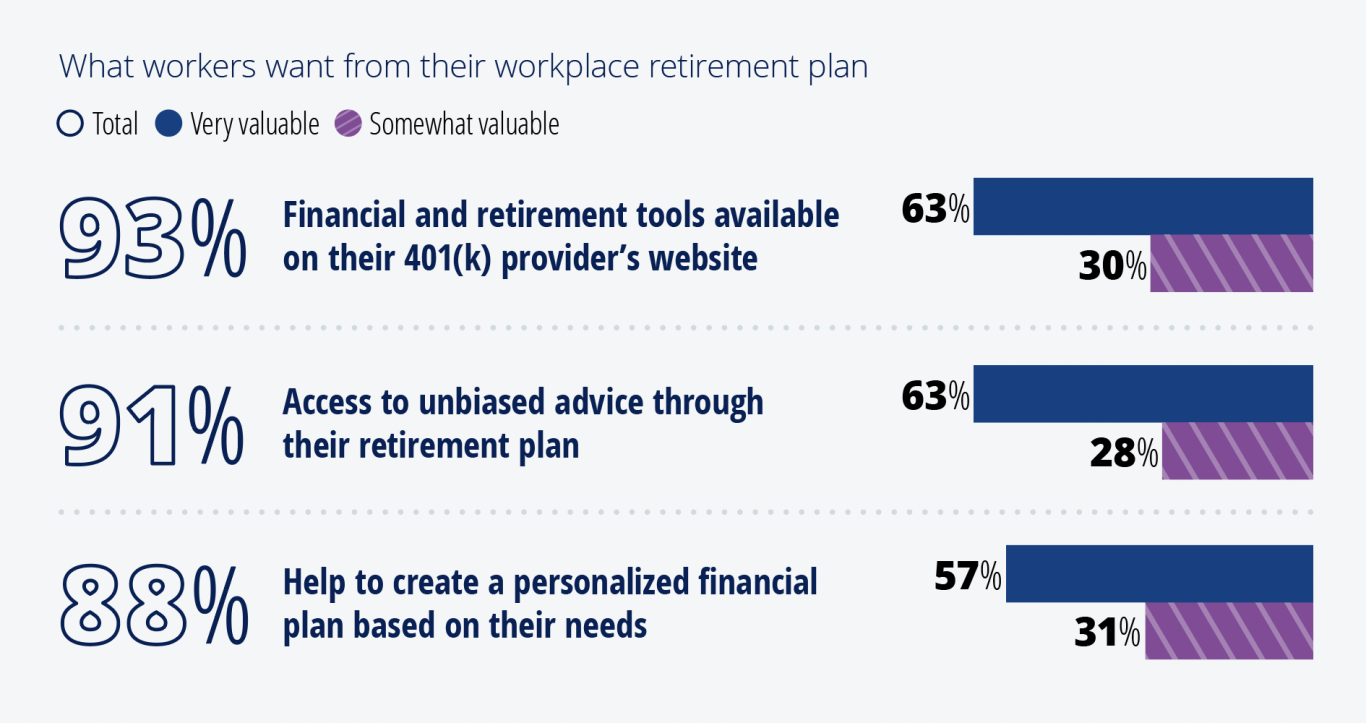

Workplace savers value online resources, personalization, and unbiased advice

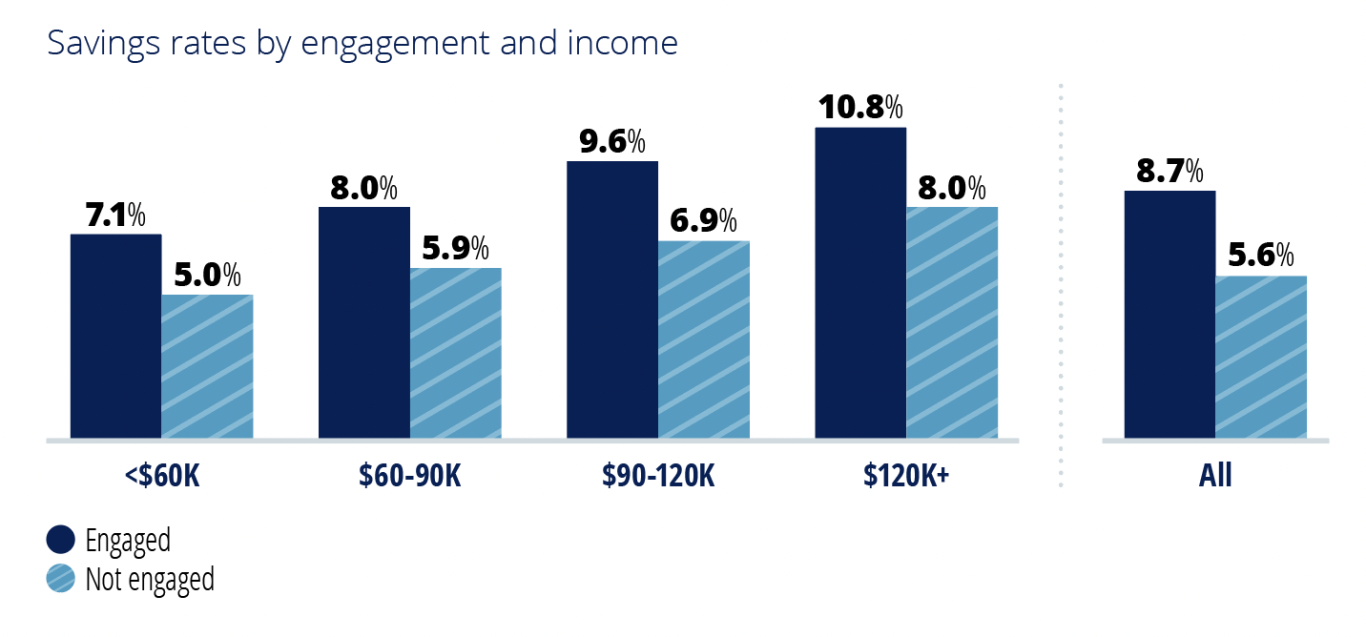

Engagement strongly correlates to positive behaviors

Engaged people save 53% more than those who are unengaged. Unengaged workplace savers are also more likely to not fully meet their employer match compared with engaged employees.

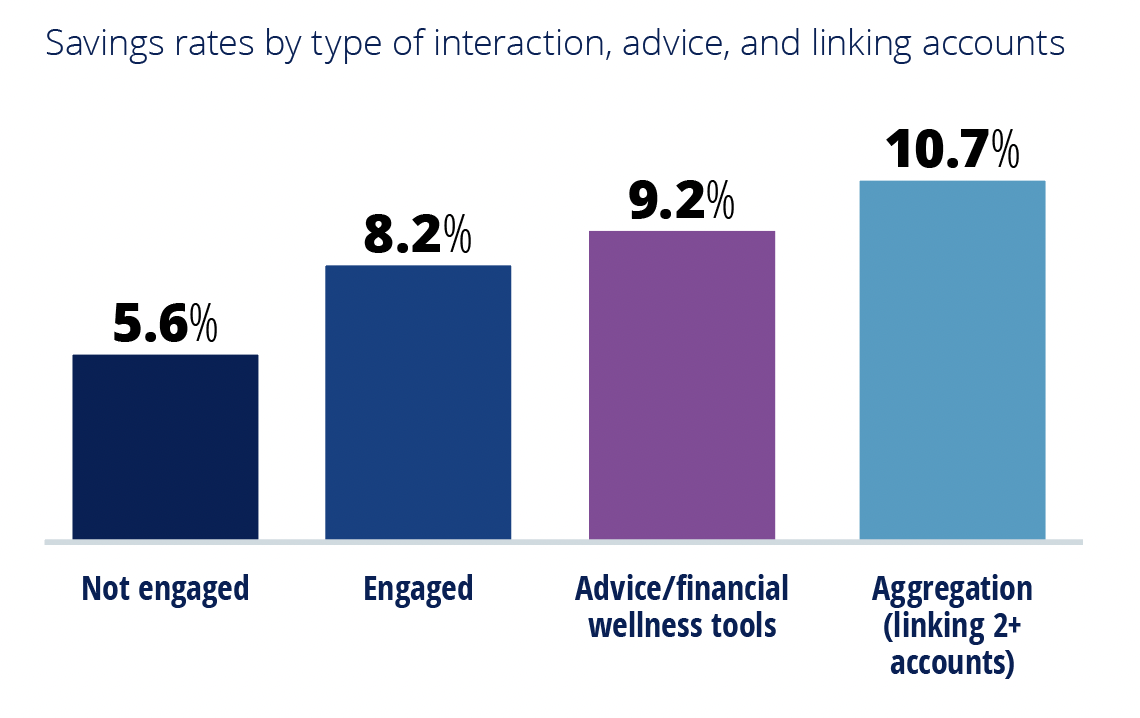

People who are engaged leverage financial wellness tools and resources, seek out advice, and link accounts save more than people who are not engaged

Workplace savers who utilize advice or financial wellness tools save 12% more than engaged workplace savers not using the same resources. And workplace savers who have linked three or more accounts save 30% more than those not linking accounts. Among workplace savers linking three or more accounts, 72% also take advantage of financial wellness tools.

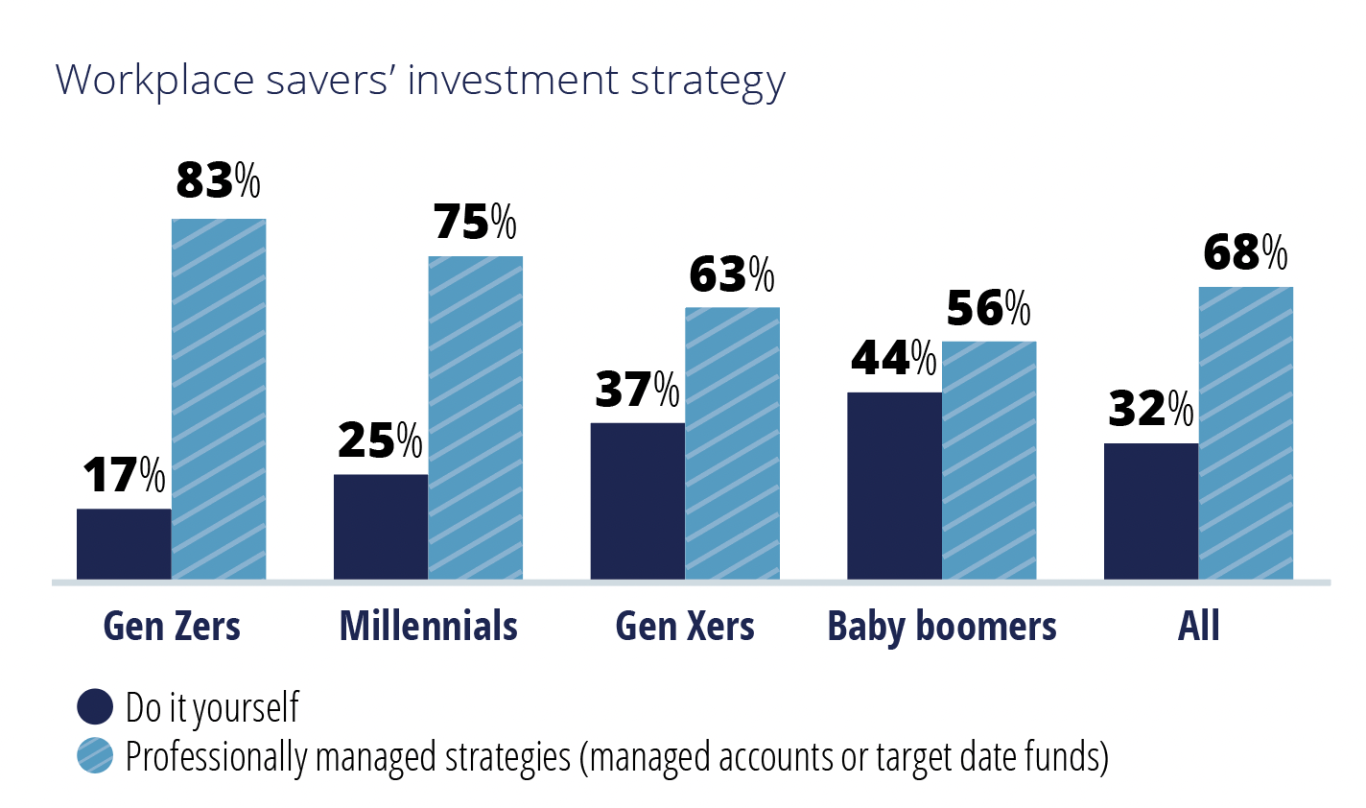

Workplace savers using managed accounts are saving 27% more and are more engaged with their retirement plans than target date fund users

The usage of professionally managed strategies (managed accounts and target date funds) is highest with younger generations.

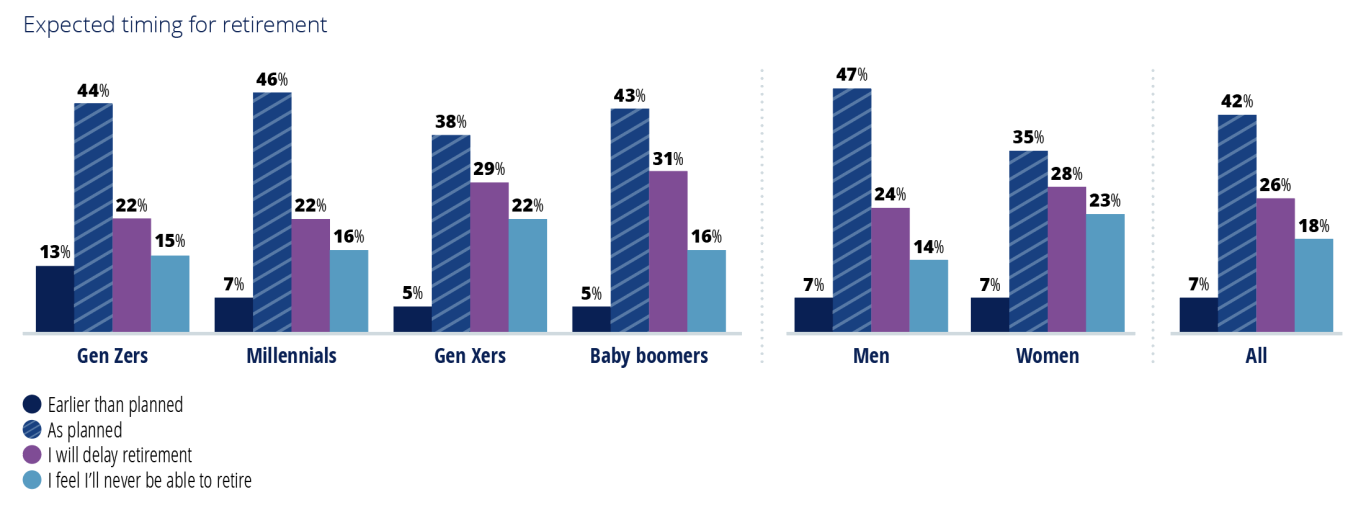

Mixed feelings about retirement timing and Social Security highlight the uncertainty felt by many

Almost half of Americans (49%) expect to retire earlier than planned or on time, but one-fifth (18%) feel like they’ll never be able to retire. Americans are also split about Social Security’s potential contribution to their retirement income: 24% don’t expect it to be there at retirement, 37% expect it to play a small role, and 31% expect it to be a primary or large income source.

Tips to empower Americans along their financial journey

Focus on maximizing retirement savings based on your financial situation and retirement goals. Consider long-term retirement savings goals and current financial realities when deciding how much to save.

Seek help navigating the current economic environment. Take advantage of the variety of resources available through your employer and retirement plan provider.

Plan for your income and emotional needs in retirement. Evaluate how much monthly income you’ll likely need in retirement and how you’ll spend your newly found free time to pursue a socially and emotionally fulfilling retirement.

Download the study to learn more

WF-3006150-1123 RO3253668-1223

The study is based on the analysis of 5.3 million active participants from primarily corporate 401(k) plans with Empower as the recordkeeper and a survey of 2,511 working Americans between the ages of 18 and 70 conducted in August 2023.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries. This material is for informational purposes only and is not intended to provide investment, legal, or tax recommendations or advice.

The research, views, and opinions contained in these materials are intended to be educational; may not be suitable for all investors; and are not tax, legal, accounting, or investment advice.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2023 Empower Annuity Insurance Company of America. All rights reserved.

Want to stay in the know?

Want to stay in the know?

Power up with the latest money news, sent every week to your inbox.

*If you’re already registered with Empower, please use the same email address as your existing account.